How to manage your finances, In today’s fast-paced world, where the cost of living continues to rise and economic uncertainties abound, managing your finances has become an essential life skill. Achieving financial stability and security not only provides peace of mind but also paves the way for long-term prosperity and the ability to pursue your dreams and aspirations.

Effective financial management is not merely about budgeting or saving money; it’s a holistic approach that encompasses goal-setting, risk management, debt reduction, and strategic investment. By mastering these principles and developing sound financial habits, you can take control of your financial future and navigate life’s challenges with confidence and resilience.

How to manage your finances : 3 Proven Strategies to Master Your Money

This article will equip you with practical strategies and actionable steps to manage your finances effectively, enabling you to achieve your financial objectives and cultivate a sense of financial well-being.

Understanding Your Financial Landscape

The first step in managing your finances is to gain a comprehensive understanding of your current financial situation. This involves:

1. Assessing Your Income and Expenses: Take a close look at your income sources and track your monthly expenditures, including fixed costs (rent, utilities, loans) and variable expenses (groceries, entertainment, transportation). This assessment will provide insights into your cash flow and identify areas where you may be overspending.

2. Evaluating Your Debt: Identify any outstanding debts, such as credit card balances, student loans, or mortgages. Understand the interest rates, repayment terms, and the impact these debts have on your overall financial health.

3. Reviewing Your Savings and Investments: Evaluate your existing savings accounts, retirement accounts (e.g., 401(k), IRA), and any other investments you may have. Assess their performance and alignment with your long-term goals.

4. Analyzing Your Credit Score: Your credit score plays a crucial role in your financial well-being, affecting your ability to secure loans, rent an apartment, or obtain favorable interest rates. Understand the factors that influence your credit score and monitor it regularly.

By thoroughly understanding your financial landscape, you can identify areas that require immediate attention and develop a comprehensive plan to address your unique financial needs and goals.

1. How to manage your finances : Setting SMART Financial Goals

Establishing clear and attainable financial goals is essential for effective money management. Use the SMART (Specific, Measurable, Achievable, Relevant, and Time-bound) framework to define your goals:

1. Short-term Goals (1-3 years): These may include building an emergency fund, paying off high-interest debt, or saving for a down payment on a home.

2. Medium-term Goals (3-7 years): Examples could be funding a child’s education, starting a business, or taking a dream vacation.

3. Long-term Goals (7+ years): These typically involve retirement planning, achieving financial independence, or leaving a legacy for your loved ones.

By setting SMART goals, you provide a clear roadmap for your financial journey and increase your chances of success by breaking down larger objectives into manageable and actionable steps.

2. How to manage your finances : Developing a Realistic Budget

A well-crafted budget is the foundation of effective financial management. It helps you allocate your income towards essential expenses, savings, and discretionary spending while ensuring you live within your means. Here are some tips for creating a practical and sustainable budget:

1. Track Your Spending: Use a budgeting app, spreadsheet, or pen and paper to record your daily expenses over a month or two. This will provide valuable insights into your spending patterns and help identify areas where you can cut back.

2. Categorize Your Expenses: Group your expenses into categories such as housing, utilities, transportation, groceries, entertainment, and debt payments. This will help you prioritize your spending and allocate funds accordingly.

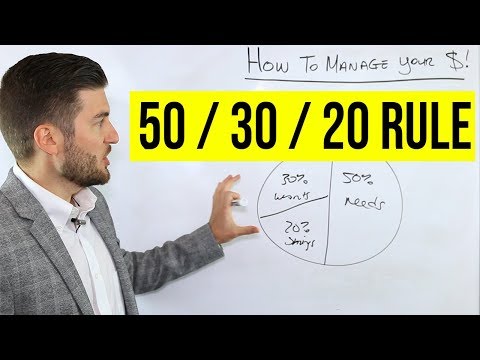

3. Implement the 50/30/20 Rule: A popular budgeting strategy recommends allocating 50% of your income towards essential expenses (housing, utilities, groceries), 30% towards discretionary spending (entertainment, dining out), and 20% towards savings and debt repayment.

4. Automate Your Savings: Set up automatic transfers from your checking account to dedicated savings accounts or investment vehicles. This “pay yourself first” approach ensures that you prioritize saving before spending on non-essential items.

5. Review and Adjust: Periodically review your budget to ensure it aligns with your changing circumstances and financial goals. Adjust as needed to accommodate evolving priorities or unexpected expenses.

By adhering to a well-structured budget, you’ll gain control over your finances, reduce unnecessary spending, and create a roadmap for achieving your financial objectives.

3. How to manage your finances : Mastering Debt Management

Debt can be a significant obstacle to financial freedom, but with a strategic approach, you can effectively manage and eliminate it. Here are some practical strategies for getting a handle on your debt:

1. Prioritize High-Interest Debt: Focus on paying off high-interest debt, such as credit card balances or personal loans, first. These types of debt can quickly accumulate and hinder your progress towards other financial goals.

2. Implement the Debt Snowball or Debt Avalanche Method: The debt snowball method involves paying off your smallest debts first while making minimum payments on larger ones. As you eliminate each debt, you can roll those payments towards the next largest balance, creating a “snowball” effect. The debt avalanche method prioritizes paying off debts with the highest interest rates first, regardless of the balance.

3. Negotiate Better Terms: Contact your creditors and attempt to negotiate lower interest rates, waived fees, or more favorable repayment terms. Creditors may be willing to work with you, especially if you have a good payment history.

4. Consolidate Your Debt: Consider consolidating multiple debts into a single loan with a lower interest rate or more manageable payment terms. This can simplify your payments and potentially save you money in the long run.

5. Seek Professional Assistance: If your debt situation is overwhelming, consider seeking the guidance of a certified credit counselor or financial advisor. They can provide personalized advice and help you develop a debt management plan tailored to your specific circumstances.

By proactively addressing your debt, you’ll free up cash flow, reduce interest charges, and create a path towards financial independence.

4. How to manage your finances : Building an Emergency Fund

Unexpected expenses, such as medical bills, car repairs, or job loss, can quickly derail your financial plans. That’s why building an emergency fund is crucial for protecting yourself against life’s uncertainties. Here’s how to get started:

1. Determine Your Target Amount: Financial experts generally recommend saving enough to cover 3-6 months’ worth of living expenses. However, your target amount may vary based on your individual circumstances, such as job stability, family size, and other financial obligations.

2. Start Small and Automate Your Savings: Begin by setting aside a small, manageable amount each month and gradually increase your contributions as your income allows. Automate your savings by setting up recurring transfers from your checking account to a dedicated emergency fund account.

3. Choose the Right Account: Consider using a high-yield savings account or a money market account to earn interest on your emergency fund while keeping it easily accessible when needed.

4. Treat It as a Priority: Prioritize building your emergency fund before allocating funds towards other discretionary expenses or long-term investments. This will provide a crucial financial safety net in times of need.

5. Replenish After Use: If you need to tap into your emergency fund, make it a priority to replenish it as soon as possible to maintain your financial preparedness.

Having an emergency fund in place can provide peace of mind and prevent you from accumulating high-interest debt or dipping into retirement savings when faced with unexpected expenses.

5. How to manage your finances : Investing for the Future

While saving is crucial for short-term goals and emergencies, investing is essential for building long-term wealth and achieving financial security. Here are some strategies to help you get started:

1. Understand Your Risk Tolerance: Before investing, assess your risk tolerance and investment horizon. This will help you determine the appropriate asset allocation (the mix of stocks, bonds, and other investments) that aligns with your goals and risk profile.

2. Diversify Your Portfolio: Diversification is a key principle of successful investing. By spreading your investments across different asset classes, sectors, and geographical regions, you can mitigate risk and potentially achieve more consistent returns over time.

3. Consider Tax-Advantaged Accounts: Utilize tax-advantaged accounts, such as 401(k) plans or Individual Retirement Accounts (IRAs), to maximize your savings and minimize your tax burden. These accounts offer tax-deferred or tax-free growth, depending on the type of account.

4. Automate Your Investments: Set up automatic transfers or payroll deductions to contribute to your investment accounts regularly. This “set it and forget it” approach can help you grow efficiently.

Watch the video : How to manage your finance

Conclusion

Managing your finances effectively requires dedication, discipline and the right strategies. By creating a budget, cutting unnecessary expenses, paying off debt, saving for emergencies and the future, and investing wisely, you can take control of your money and work towards achieving your financial goals. It’s an ongoing process that requires regular monitoring and adjustments as your circumstances change. However, the effort is well worth it for the financial security and peace of mind it can provide.

FAQs:

1. How much should I save for an emergency fund?

Most experts recommend saving enough to cover 3-6 months’ worth of living expenses in an easily accessible account like a savings account. This provides a cushion for unexpected events like job loss or major repairs.

2. What’s the best way to pay off debt?

The “debt snowball” and “debt avalanche” methods are two popular strategies. The snowball method has you pay off the smallest debts first for motivation, while the avalanche method focuses on paying debts with the highest interest rates first to save money over time.

3. How much should I save for retirement?

A general guideline is to save 10-15% of your pre-tax income for retirement, including any employer match. The specific amount depends on your desired retirement lifestyle and age you plan to retire.

4. What types of investments should I consider?

Common investments include stocks, bonds, mutual funds, ETFs, real estate and retirement accounts like 401(k)s and IRAs. The right portfolio depends on your risk tolerance, time horizon and financial goals.

5. When should I consult a financial advisor?

A financial advisor can provide personalized guidance, especially for major events like inheritance, career changes, divorce or retirement planning. They can also help manage complex investment and tax strategies.

Must read : How to enhance your research skills

How to enhance your research skills : 3 Powerful Strategies to Become a Research Ninja